Your Home Buying Guide

Hello, My name is Matt Ward. I am a Realtor with Delicious Real Estate in Columbus, Ohio. I am a father and husband who began a career in Real Estate to allow me to choose my own schedule so I can spend more time with my son, Sam. I also spent 10 years as a full-time stand up comic. I got into Real Estate after having two less than satisfactory experiences when buying and selling my first home. Now I use my humor and problem solving to help you navigate the process of buying a home. I have one rule, respect my time and I will respect yours.

I am also a video producer. I create videos about affordable housing all over the country on Tiktok, Instagram, Reddit and Youtube. If you check out that content you will really get a feel of who I am.

First, a reminder about my contact information:

mattward@deliciousrealestate.com

614-805-2231 Mobile OR 614-333-5304 (desktop number)

My Service Area

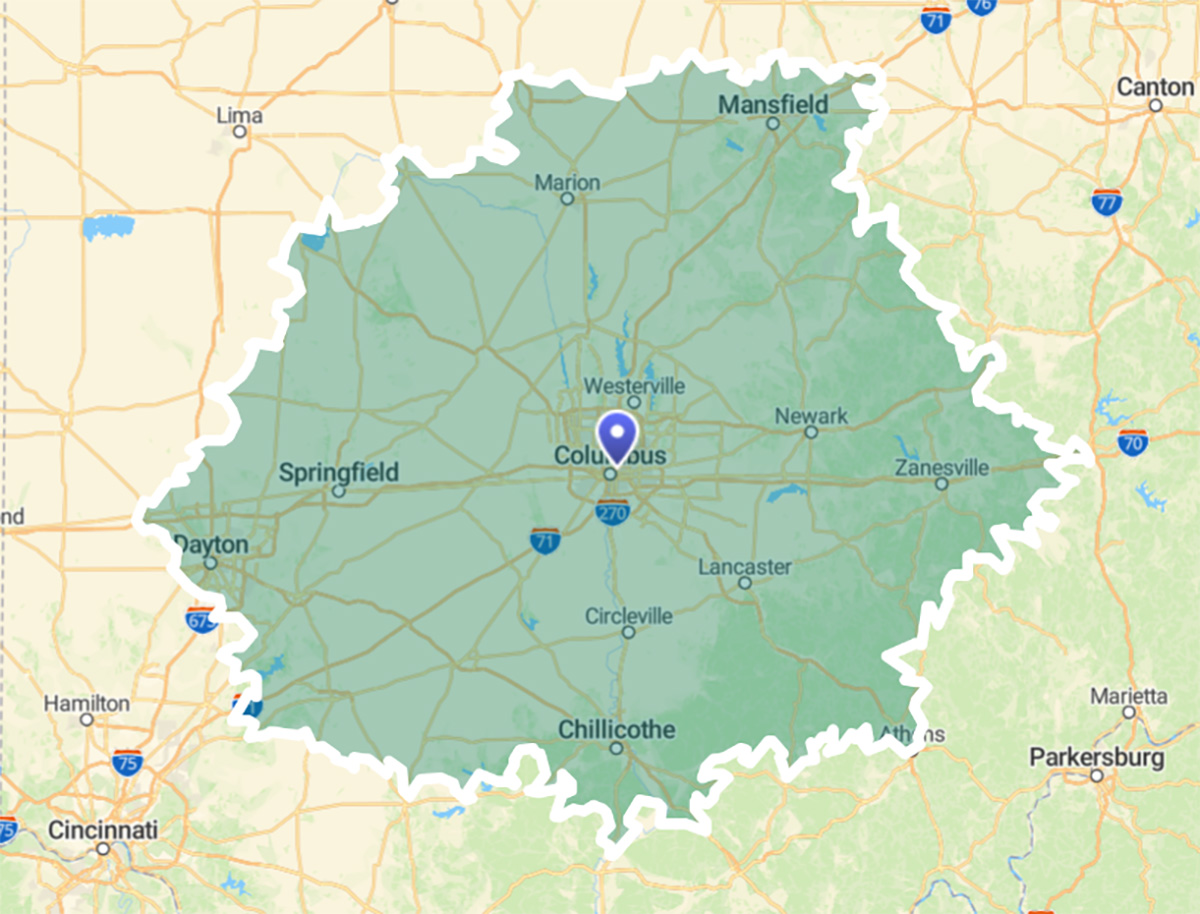

I live in Westerville, Ohio, a Northeast Suburb of Columbus, Ohio. I am licensed to sell Real Estate ANYWHERE in the State of Ohio. However, I have a large network of agents ALL over the country who I have vetted and trust. This means if you are looking to buy a home outside of Ohio, I can likely refer you to someone trustworthy to help you with this.

My office is located in the King Lincoln neighborhood of Columbus, Ohio. I don't spend a great deal of time in my office, as I am typically working from my home office in Westerville.

In terms of what areas I cover in Central Ohio, it's pretty much a one hour fifteen minute Circle around Columbus. I have sold in the following Counties in Ohio: Athens, Delaware, Fairfield, Fayette, Franklin, Licking, Meigs, Muskingum, Perry and Union.

I do not cover Cincinnati, Dayton, Toledo, Akron, Cleveland areas. I will refer you to someone else if you have interest in real estate in those places.

Step 1: Financing

Lenders - Mortgages and Pre-approvals

Get Pre-Approved

What is a pre-qualification? A ‘pre-qual’ as they say in the real estate biz, is simply a letter from a lender saying you are approved to borrow money from them for a home purchase based on the quick snapshot of your finances. Get it as soon as possible. Most buyers pop into their local bank where they keep their checking and savings accounts and accomplish the pre-qualification quickly and easily. If you don't have a pre-qualification, you can also touch base with one of the lenders below and get one ASAP so we can put that behind us. Remember that what matters is not the dollar amount you're qualified for but how comfortable you are with your MONTHLY mortgage payment. Come up with an idea what the most you want to pay monthly is and express that to the lender up front.

Choosing a Lender

Not all lenders are the same, though many of them offer similar products (thanks to federal guidelines). In general, it is my preference that you use a lender that is local and small. Why local? Accountability skyrockets when the lender is local. Why small? Small because at the end of the day you want to be able to walk into an office and meet most of the people making a decision about your financial future. When there is a problem with underwriting, my preference is that your loan officer can walk down the hall and talk to the underwriter, not leave a message on a voicemail several states away.

Also, different lenders excel at different things and if you are bringing a relationship with a lender to the home search, by all means please continue with that lender. If you are open to a different lender, I will recommend some I work with frequently and who always get the job done.

Once we find a home and make an accepted offer that is when you can shop around for the lender who is going to be the one to process the loan for you. It’s always wise to check out at least three different lenders for this to shop rates and available programs. This way you can compare real apples to apples on loan products and programs. Below are a few lenders I have worked with multi-times who have never failed me. Both are excellent with communication which is the most important thing about a lender.

Ian Eichelberger - Cross Country Mortgage P: 614-493-7116 E: ian.eichelberger@myccmortgage.com | Michele Rodriguez - Union Home Mortgage P: 614-410-9133 E: michelerodriguez@uhm.com |

How much money should I have saved up?

The amount of money you will need to close on a house varies greatly. In a seller's market you must pay your own closing costs which can be higher than $3800-5000. The seller also has closing costs of their own, you are not required to pay these but in the peak of the market buyer’s were offering to cover the seller’s closing costs. Your down payment will depend on the loan. For Conventional loans you would need either 3 or 5% down. If FHA it is 3.5% down. VA and USDA have no down payment.

DOWN PAYMENT ASSISTANCE: There are programs that help with down payment assistance but they will result in a higher monthly payment and typically a second mortgage on the borrowed funds which hate to be paid back on part if you leave before 5 or 7 years. There are also programs that do no require a down payment that don’t require a second mortgage so just ask me about those because they change all the time.

Please consult with your chosen lender about your “Cash to close” amounts which will vary by offer amount. If you are bidding in a very competitive sellers market you may also need funds for an appraisal gap. Those funds are above and beyond the closing costs and down payment. We will touch on appraisal gaps later.

Step 2: The House Hunt

What to expect while we house hunt

I'm your go to for all real-estate-related matters/showings/walk-throughs. Where can I show a house? Anywhere in Ohio, except Portsmouth. Oh yeah, and I am still not allowed back at Put-In-Bay, but everywhere else I can help you. Mostly I show houses within 90 minutes of Columbus.

Regardless, DON’T use the contact form on your favorite real estate app, simply use the forward button instead and send any listing that catch your eye to me via text and I will find out more about it and give you honest feedback or set up a showing. (If you use the contact form it goes to another agent who will then try to make you their client, ain’t nobody got time for that!)

If you have a question, call/text me and I will do my best to answer it. I don’t make up answers. If I don’t know, I will say I don’t know and go find the correct answer.. Don't worry about 'bothering' me, you won't. If I am unavailable or with family I may let you know but will also give you a timeline for when I will be available to chat further. Text is best, much better than e-mail for me. Helps me keep conversations documented and details straight.

Real Estate Apps: Most people use Realtor.com’s app as it is sponsored by the National Association of Realtors. I prefer Redfin for searches in the Central Ohio area. It does two things I like better than Realtor.com’s app. 1.) Redfin updates quicker with listings showing up in minutes whereas Realtor.com is sometimes hours 2.) Redfin gives you a handy breakdown of what your monthly payments would be and lets you customize this to change the down payment or interest rate. What about Zillow or Trulia? I don’t recommend either because of the amount of incorrect data that these apps show. They are slower to update when houses go in contract for example. Use Redfin. Forward me the listing that catches your eye from there.

So now you have your app and your beginning to search the areas you like in your preferred price range. Perfect, do this all the time. Favorite properties you like and the app will notify you when the status or price changes. You want to search for Active properties. When a house goes Contingent or Pending, both mean that the seller has accepted an offer from a buyer.

Direct Search through the MLS

I will set up a search for you too! Since I am a Realtor I have access to the Multiple Listing Service aka the MLS in Central Ohio. Everything that is listed on the open market first comes to the local MLS before it propagates out to Redfin, Realtor.com, Zillow and dozens of other sites. I can set this up for you as well. The advantage of a direct MLS e-mail search is that I can filter out things you cannot filter out on the consumer apps like whether the home is an auction property, or accepts certain types of financing for example.

So how do showings work?

So you have found some houses you want to see, now what? Text me with the addresses of the properties you want to see and the time and day you are available to see them. I will verify that I am available and that the property can be shown at that time.

I typically schedule showings through Showingtime, the primary local showing portal. There are two general types of statuses.

Go and Show: Meaning the house is quickly able to be shown and auto approves.

Appointment Required: This is when either the seller or the agent have to approve each showing request that comes in.

Either way, a showing with me is never confirmed until you receive an e-mail link with a Google Calendar invite from me, followed by a text confirmation. This helps us easily store the showing schedule in our phones with the pertinent information so we can navigate from showing to showing. Please note, I typically DO NOT drive my clients around to showings, but if this is something you would prefer, I can make arrangements.

It's OK to fall in love with the first house you see. It'll probably feel awkward if you make an offer on that house right away - trust your instincts and trust your agent on whether or not you're making the right decision on this particular house because we know the market and bring more knowledge to the table than you can be expected to have. (But you know what you like and you've probably already been watching the market for a long time before you reached out to me) If you feel like you simply must see more houses and you want to keep the first one on the back burner, I completely understand but be prepared to lose it because someone else will like the house for the same reasons you do.

The house that you start off wanting might not be the house you end up buying. It's OK. Often my buyers end up purchasing something completely different than what they set out to buy -- but they are happy with their choice. It's important to be happy with your choice. We're talking about YOUR home here. Try your best to balance the emotional and logical parts of your brain. They will likely be at odds through much of your search. Yes, it is an emotional roller coaster at times, especially in this competitive buyer’s market, but we will succeed in finding you what you want, it just may take some time.

Chances are good your perfect house doesn't exist. As your home search goes on you will notice that you are mentally rearranging what aspects of a home are more important to you. This is absolutely normal. Actually viewing homes in person is very different than just seeing them online. Sometimes a home gives you a feeling that makes many of your ‘deal breaker’ items seem much less like deal breakers. This is where you are back to balancing your emotional and rational self. I will help you by presenting the pros and cons as I see them in as unbiased manner as possible.

How many homes will we look at?

You probably won’t find the home you want within three showings. How many will it take? It's hard to say. I've had buyers look at only one home with me after months of online searches on their own and I've had buyers who I have shown dozens of homes. The national average is 12. I find that the average for my buyer’s is about 20. Typically we should limit the number we see in one day to about five. Anything more and they run together for you.

It sounds cliche, but when you see the right house, you just know. It's not a divine miracle. The reason you 'just know' is that you have seen enough homes in person and online to understand the price-location-condition equation in the geography you want and when you see something that offers the right combination of the above you know.

Is this always the case - no, because sometimes the market is so crazy that every offer is a mad rush with lots of other offers and you might lose a few of these houses to other buyers. You might find yourself buying a house you don't love just to get it over with or to meet a deadline (your lease is expiring and you have nowhere to go) - this happens and isn't the ideal situation. I usually try to talk you out of that house but I find you'll quickly learn to embrace the odd and grow to love whatever house you purchase.

When you find the right house, don't delay. It never fails that even if the house has been on the market for eight months, the minute you want it so will two other buyers. If it came on the market in the morning and you see it in the afternoon and it's the one, don't delay - act as quickly as possible. Make an offer. You need to be the one in control of the purchase of the house. Being first is always best - you have more negotiating power because you're the only buyer.

Ok, I want to offer, now what?

This is where it's time for us to have a discussion about what I think would be the best strategy for you to get the house you want for a price you are willing to pay. It takes me about 14 minutes to write an offer from scratch. I carry my laptop everywhere I go so I can write an offer from anywhere at any time. I will give you my recommendations on the offer, write it up and electronically send it to you to e-sign. Once you have signed the offer digitally I will present it to the listing agent. This offer will include an expiration day and time, meaning the amount of time we are giving them to accept our offer or counter. (Seller’s market note: When it has been communicated that multiple offers have been received on the property you are interested in, the agent will also typically communicate an offer deadline day and time.

What happens if the house has multiple offers?

Here is my general rule of thumb when it comes to offers. For the sake of simplicity let's say our subject property is listed at $240,000. How do we know what we will need to offer? Well, that depends on how many other offers are received or expected. Below is a breakdown of offer strategy based on the number of offers received.

*No offers received- Provided the home has been on the market for longer than 48 hours, we can ask for your closing costs to be paid and offer list price or less.

*1 other offer already received- Then we are not going to be able to ask for closing costs and our offer must be list price or better.

*2 other offers already received- Well then we are escalating rapidly. To be competitive you would have to offer $145,000 or higher, not ask for closing costs and likely waive one of your contingencies (Waive Repair Request is the most common waived contingency).

*3 other offers received- This means this will likely get pushed up to $255,000 As-Is (meaning you can have inspection but can't ask for repair) Waiving seller paid home warranty and giving the seller up to 30 days of additional possession after closing if requested). At this point it is likely the seller is going to want some protection in the event that the house doesn't appraise at the contract price. This is commonly referred to as an 'Appraisal gap clause'. More on the appraisal gap clause in a minute.

*10 or more offers- believe me this happens more often than you would think. I have won in 10 offer situations multiple times but it becomes much less likely. This is because once you get around 10 offers you're almost guaranteed one of the offers is cash. Cash is king in that there is no appraisal needed and the buyer can close in half the time it takes for someone with financing. So how exactly are you competitive in a 10 offer or more situation?

You must

- waive any request to remedy, provide a larger earnest money deposit, offer your maximum appraisal gap,

- waive the seller paid home warranty,

- provide proof of funds that you have the $$ for your down payment, closing costs and appraisal,

- must give the sellers as much possession time as they are requesting

- must close sooner than other offers.

Then after all that you still only have a 30% chance of winning. Like I said, cash is king and we have parents in the suburbs with deep pockets providing cash loans to their children to buy and institutional investors (you know, the real scum bags) who are buying cash and turning the homes you are offering on into rental properties…

What is an appraisal gap clause?

An appraisal Gap clause is a clause and a purchase contract where the buyer agrees to give up to a certain amount of cash above and beyond their down payment and closing costs to the seller as part of the purchase of the home.

Example:

"In the event of an appraisal below the contract price the buyer agrees to bring a maximum amount of '$5000' to the closing table to help make up the gap."

So your willingness and ability to offer this type of coverage in the event of multiple offers depends on the amount of cash you have available.

Let’s go back and use the $240,000 house we offered $255,000 on as an example. We would have likely had to offer at least $5,000 in appraisal gap. Let’s say this property only appraises at $240,000. Oh boy, the bank will only loan up to the amount of the appraisal and no more, so two things are going to happen, you are going to have to increase your out of pocket by $5,000 and the seller is going to have to lower the purchase price of the property.

Extended Possession:

About half the time in a multi-offer situation the seller wants extended time after the closing where you've paid for the home but they continue to live in it. I have listed two homes in the last year where the sellers have gotten an additional 30 days to live in the house after they were paid for it. During this time they will continue to have the utilities on and in their own name but you will have the property insured and interest will begin to accrue on the mortgage. This is a very common buyer concession.

Can the Seller Blow Off my Offer/Deadline? While it seems counterintuitive, yes they can. You're the first one to see a house you've been waiting for, you make a full price offer immediately - it's exactly what the seller asked for --- then the seller says they won't get back to you by noon because they want to wait until anyone else who wants to see the house has an opportunity to see it - and write more and bigger/better offers than your measly list price offer, leaving you out in the cold. It's awful and it happens all the time. While being first is always best, it doesn’t always have the same weight when market conditions favor the seller as they currently do.

Is this a safe neighborhood? I cannot, by law, speak to the safety or makeup (by income, race, family status, etc) of any particular neighborhood. I will do my best to answer any questions you have about a neighborhood, especially in regard to real estate-specific questions, but I urge you to do your own due diligence to make sure that after you buy the home you feel happy, comfortable and SAFE in it.

The BEST thing you can do is walk the streets of the neighborhoods you are interested in. Nothing lets you know how comfortable a neighborhood makes you feel like shoes on pavement seeing it all for yourself. Also I recommend for areas you are not sure about to drive the area at night. You want to

Pay Attention to The Status of a Home When Looking

It’s important to check the box on your app that hides pending or contingent listings. The only properties you should be interested in are ones that are ACTIVE. If a buyer writes an offer on a home that is accepted, the listing agent has 48 hours to change the status on the MLS. This DOES mean that occasionally homes show active that have an accepted offer very recently.

Coming Soon- This means a listing agreement has been signed by the seller and the agent is now required to input the information about the home in the MLS (Multiple Listing Service) so other agents and buyers can see that the property will soon be active. A property can be Coming Soon for a maximum amount of 30 days. During the coming soon NO SHOWINGS are permitted, but offers may be placed site unseen (often referred to as ‘curb’ offers). This is why sometimes you will see a home is coming soon, then it goes into Contingent or Pending Status before it ever begins showings.

Active - The home is for sale and if showings are allowed (not curb offers only) it will be possible to schedule a showing provided the schedule has not filled up. There is no required time that a property must accept showings. On competitive properties it is imperative to make yourself available the first day showings are available. If the property shows coming soon, schedule in advance for the first active day on the market.

Contingent Finance & Inspection - Another buyer has put the home in contract and the home is sold contingent on the buyer having a satisfactory inspection and contingent on them getting their financing.

Pending - Although sometimes used in Lieu of contingent on Financing and Inspections, This is supposed to be used once the home is in firm contract and parties are past the inspection phase and the buyer's lender has produced a letter of commitment to lend on the mortgage - This home is SUPER In CONTRACT and highly likely to close. Also, PENDING is the status used when the seller accepts a cash offer.

Step 3: The Offer

Get to know the purchase contract

While it's true that we just sit down and 'fill in some of the blanks' on the purchase offer, it's important to read through and understand the document. Many agents whip one out at the time of making an offer but I want to make sure you've had ample opportunity to read this and ask any questions that you may have. It's important that you're comfortable with this important document.

Regarding time-line dates in the offer, I typically use the following:

- Time for the seller to respond to your offer - this is often situational. If possible, it's nice to give them a night to sleep on it but my preference is for a quick response - as quickly as seems doable so that no other buyers have the opportunity to make an offer before the sellers respond. So, usually by 8pm same day or noon the next day, 6 pm if they simply can't do anything but work at work. No matter how long a house has been on the market, it never fails that as soon as you have interest in it, so do others.

- Days from the day of the offer to the day of the closing (keys in hand)--Conventional Loan 4-5 weeks, FHA Loan, 6-8 weeks.

- Days for the inspection period: 10 days is usually enough and then an additional 5 days to go back and forth about what will get fixed and what won't get fixed.

- Time for possession - my preference is always to have possession of the house as soon as the closing is over if at all possible. On occasion a seller will request some time from the close to move. This is laid out in advance and agreed upon during the contract negotiations.

Disclosures

Everyone has to cover their ass and you need to know who represents whom in a real estate transaction - you need to know about the dangers of lead paint and you need to know what the sellers have to say about the condition of their home.

That last disclosure, the Residential Property Disclosure, is house specific and comes from the seller. Don't write an offer without seeing what is revealed on that disclosure. This is the disclosure that the seller gives to the buyer that outlines everything that they know to be wrong with the property. This is a state required document. If you do write an offer on a home without seeing this disclosure, make it contingent on your satisfaction with this document.

This is a required form that says whether or not the seller knows there is lead paint in the house. (If it was built before 1978, it has lead paint in the house. Unless you scrape the paint off and send it to a lab, you don't really know so it is very rare that a seller discloses lead paint. This is a federally required document.

This is my company's policy regarding who works for whom - Delicious Real Estate is one of the Only Brokerage in the City that has a strict policy of not representing both sides of a transaction. Your agent will only represent the buyer or only represent the seller. This is also a state required document that I have to give you pretty much immediately. Likely I will send this to you for electronic signature soon so that you can get in and be familiar with that online system before it's urgent.

What to expect as we ready to write an offer

If you're serious about a house, make a serious offer. Lowball offers only make sellers unhappy and make you look like you have no idea what you're doing. While you're playing around with a lowball offer some other buyer will swoop in with a better one and the seller will want to deal with them and not you. If there are other offers coming in or on the table, consider the idea that you may (likely will) be paying a purchase price above the list price. The average sale price/list price in all of Franklin County from March 1 - August 31 2016, for example, was 98.2%.

That said, if the house is overpriced, it's overpriced and you need to make an offer based on reality -- not future potential or seller vanity. Let someone else over-pay for a house. In some markets (the Short North for example) listings are rare and just as rare is a home that goes out below list price in a Seller's market. People over-pay by tens of thousands of dollars because they are banking on the home out-performing all other areas in terms of appreciation for the foreseeable future. Every once in a while, it's OK to overpay because you just like the stupid house so much you want it and you see yourself there for a long time - but do be prepared to bring extra money to the closing table if the appraisal comes up short.

Be Flexible on Possession Dates. Conventional wisdom says to expect to close on the house about 30-40 days after the day you wrote the offer. Add 2 weeks longer if it is an FHA loan or there is something out-of-the-ordinary involved like a 203K or 'fix-up' loan - you'll need contractor estimates for or a grant from a 3rd party you'll have to wait on.

Remember that possession can be something to negotiate around instead of price. Some sellers can't imagine any other scenario than staying in the house for 2 weeks after the closing to pack and move now that it's over. Can you wait two weeks? Two days or a weekend? It might help you get the house.

Overall I advise possession at closing in all deals and anything more than about ten days, in my opinion, means that the Sellers should now be paying you rent.

Multiple Offers - Yours and others at the Same Time If you're buying a house in a Seller's market, be ready for multiple offers multiple times. Homes often come on the market, are inundated with would-be buyers in the first couple days and are in contract by day three - especially in all the most desirable midtown Columbus areas. How can you increase your chances of the Seller picking your offer from the multitude?

- -Be ready emotionally for a multiple offer situation. You might not get the house, be as OK with that as you can from the beginning. While you're letting go of the outcomes, remember you can't compete with some things - like a cash offer.

- Cash can be King. It's not magic, but cash offers will often be considered above any other offer that involves getting a mortgage. The Seller will take a higher offer over a cash offer because who doesn't want more money - unless it's close, then they'll take cash because this allows them to breath easier - too many things can go wrong with mortgages and appraisals, etc. Also, if they are turning around and buying their own house, the seller of that house will have more confidence that their transaction will happen.

- -If you can't come up with the cash, Make sure you are getting a conventional mortgage, not an FHA. You'll appear a stronger buyer and a seller will take a conventional buyer over an FHA buyer every time. With programs like 5% down conventional loans with no PMI out there on the marketplace, it makes sense. Also, with an FHA loan, the seller may be required to scrape and paint areas that are peeling, or add a hand-rail, or all other manner of FHA requirements. If you can only qualify for FHA or that is your preference - no problem, we will make it work.

- -Use an escalation clause in the offer. That looks something like, "The Buyers' offer is $194,500 but they will meet and exceed any other any other by $1,000 up to and including an offer of $201,500." In this scenario, the most you'll pay is $202,500 but you could pay anywhere from 194.5K--202.5K. The point is you don't over-pay by a lot since you can't know the offer price of other people, you don't want to jump right to $201,000 if $195,000 is enough to be the highest offer.

- In the above scenario, stick to your guns - draw your line in the sand of purchase price and stick to it and be fine walking away from the house at anything above that price. You can't beat yourself up later with, "If only we'd gone another $1000 that might have made a difference."

- -Be generous on the time of possession. If you close on March 31, maybe the sellers would like to close on the house, turn around and close on their next house the next day, and take five days including a weekend to move out of the house so give them that extra week to get out of your house. -But, more than ten days and I usually suggest talking about the idea of them renting back from you. If you're flexible and it's important to them, it can make a difference.

- -I recommend writing that letter that talks about who you are, how much you love the house and how much you'll enjoy living there and in the community and bringing up your family in the house, etc. Have that written and ready to go so you can just make a few relevant tweaks for the particular house. I want it to make me cry because it's so beautiful. It's not hard to find out a thing or two about the sellers on Facebook or other places, tailor your letter.

- Go outside the box. Make your offer stand out - for example, maybe by offering the sellers free pizza for a year. One $20 pizza a week for 52 weeks costs you the same as an extra $1040 but it makes your offer stand out and has a lot more sentimental value than that extra $1040 might - maybe you spell out that it's from the favorite local joint that you know they'll miss when they move to a different neighborhood or you know where they're moving and you Yelp the favorite joint in that community, etc. The point is, stand out and get them to like you. Do a little Facebooking and find out what they might like and what's important to the them.

- More practically, avoid contingencies others will have in their offer. You've gone through the house and you love it. You and your agent think that, from your limited perspectives, there probably won't be any deal breakers in regard to condition so you spell out in the offer that the offer is contingent on inspections but that you won't be asking for any repairs. You'll still have your inspection but only to satisfy yourself as to condition - if you do find a deal breaker, you can still exit the contract but the seller feels good that you won't be asking for any repairs. Sellers like As-Is offers.

- In a super competitive place with a little cash to play with at closing? - consider waiving an appraisal contingency altogether or tell the sellers that you'll cover the first $X,000 of a low contingency. When other offers have an appraisal contingency, they'll appreciate your offer.

What is a backup offer? Let's say you saw a home you liked and you made an offer. There were multiple offers, yours was one of 5 total offers, and you didn't get the house. Some other buyer went in contract with the sellers. Their offer is in first place. The sellers, not wanting to leave anything to chance, will likely ask all the other parties who made an offer if they'd like to be a backup offer and have their contract be in 2nd place (or even 3rd).

Buyers in this case would still make an offer and negotiate terms and sellers sign the offer. It's an official contract that has a clause that says should the first place buyers no longer be in contract (for a variety of reasons, most often buyer's regret and home inspection findings) your 2nd place contract immediately goes to first place and you are now the buyers in line to buy the house per the terms of your previously negotiated contract.

You may cancel your backup offer at any time (provided your agent put such language in the contract) should you find another house you like and go in contract on that house - So there is no real downside to making a backup offer. Often Sellers use the fact that they have a backup offer as a reason to not make any repairs the first place buyers may ask for - why should they when they have someone else waiting in the wings to swoop in and buy the house. Post Inspection Buyers, knowing there is a backup offer in 2nd place, typically ask for nothing -or less than they might have- as their negotiating power is compromised.

Step 4: An Accepted Offer

Holy Cow! Mini-Congratulations!

#1 MOST IMPORTANT THING HERE. SCHEDULE YOUR CLOSING DAY OFF FROM YOUR JOB!!! AFTER WE GO IN CONTRACT I WILL SEND YOU A TIMELINE WITH DATES. THE CLOSING WILL HAPPEN DURING THE DAY 9AM-5PM AT A TITLE COMPANY IN THE AREA OR MY OFFICE. YOU HAVE TO ATTEND TO SIGN IN PERSON. MAKE SURE YOUR ID IS NOT EXPIRED!

Upfront expenses: You may be asked to provide an earnest money check (as outlined below) in addition to this you will spend between $350-675 on inspections (depending on who you use and which ones you get) and $500 or so on the appraisal of the home. These are all up front costs. Only the earnest money is returned to you if you end up not buying the property.

Contingencies and Timelines. While you were studying the purchase offer above, you likely noticed that our offer is based on several contingencies and has several dates specified by which actions need to occur. Once the offer is accepted, it's our job to make sure we meet all timelines and all contingencies are met - at least as much as we have any control over. You need to be very aware of these timelines.

Pre-Approval Letter In a perfect world, we submit this with the purchase offer so we satisfy this contingency right away. You really have no business making an offer without a pre-approval from a lender to begin with and the seller wants to be sure you're qualified to buy their house before committing to your offer. Worst case, this should never go past three days. We can always get an updated letter from your eventual lender after you shop it around.

What if you're buying with cash? You will need to submit a proof-of-funds to the seller showing you have the Benjamins to back up your offer - bank account - investment account - 401K account - be sure you or I blackout any personal account numbers or social security numbers.

Loan Commitment We are going to ask your lender to submit a loan commitment letter or email about 30-40 days after acceptance of our offer. Maybe 45 days for an FHA loan. They will balk at that but they will do the best they can to make that happen. Sellers rarely ask for one but you should be on top of it anyway.

Earnest Money

Why: Earnest Money is an amount that you as the buyer bring forward to show the seller how serious you are about buying this particular house. It is not a requirement in the State of Ohio, or in the contract, but it is an expected part of transaction in Central Ohio.

Better you name the amount of earnest money than the seller - that way you are comfortable with the outlay.

How: Make your check out to your Real Estate Company. In our case, make your check payable to Delicious Real Estate. It will be cashed and deposited in the brokerage's trust account where it will sit until closing and the brokerage will return it to you at the closing. Often, you then endorse that check to the title company which means that ultimately your earnest money deposit simply becomes part of the closing cost monies you need to bring to the closing.

When: There are three points in the transaction that the earnest money is given to the (usually) buyer's real estate brokerage. The first is with the offer - this is usually not done because the seller may not accept your offer and the check for the earnest money becomes useless. The second, and most common, is 'upon acceptance' of your offer. This is generally taken to mean within 24 hours of your offer being accepted, so that day or the next. The third, and increasingly more common point, is post inspection period when all remedies have been agreed to and everyone is moving forward together. This takes the possibility of a contentious fight over the earnest money out of the picture.

Home Insurance

In order to purchase your property, your lender will require that there be a homeowners insurance policy on the property as of the day of the closing (condos generally have their insurance paid by the association but you should still get renter's insurance). Many people shop this around a little and many others simply call whomever has the policy for their automobiles for a multi-line discount. You should get a homeowners insurance quote right after going into contract and provide the quote to the lender you end up using. If you want to shop around, here are two trusted insurers:

John Horvath

Neverman Insurance

440-871-5620

john@nevermaninsurance

Step 5: Having the home inspected

The first thing to remember here is your inspection timeline. Typically, you have between 7-12 days to have any and all inspections done that you would like.

I absolutely recommend having a whole home inspection - this is an inspection of all facets of the house by a licensed home inspector who can point out the obvious and the not so obvious. I suggest at least one person who will be living in the home attend the home inspection - You don't have to follow the inspector around and watch everything he/she does but if they find something of interest, they can show you in person.

You also might want a Wood Destroying Insect Inspection. Termites are an actual problem, even in Columbus, Ohio -- not to mention carpenter bees and carpenter ants. Knowledge is power and if you can ask the Sellers to treat the problem, better them than you.

If you are buying an older home in an historic neighborhood around the city core, than you should consider a sewer scope. Installing a new sewer line is an expensive project ($10,000 or so) and if you're going to need one because yours is 115 years old and crumbling, you should know it going into the purchase.

Most other inspections will stem from the whole house inspection. Home Inspectors are jacks of many trades but masters of none and often their suggestion begins and ends with having a professional (plumber, electrician, roofer, engineer) take a further look at any questionable areas of the house.

Here are some Inspectors I often work with and I feel good about, but don’t worry, I can’t schedule the inspections for you.

Terra Firma Property Inspections

Linkhorn Inspections

INSPECTIONS FAQs

Who sets up the inspection - I schedule your inspections. You just have to tell me which inspections you would like to have performed. I will take care of the scheduling and attend the inspection if possible.

How much does a home inspection cost - Budget somewhere in the neighborhood of $300-675 and about 2-3 hours for the inspection. Wood Destroying Insect inspections are quick and cost about $75. Sewer line scopes are also quick and run about $250-300, sometimes less. Radon Inspections run about $125-180. Depending on the home we may recommend that you get all of these types of inspections. Consult with me and I will tell you what I recommend. General inspections usually cost between $300-400.

I'm buying a new build home, should I still have an inspection? Absolutely. I guarantee there will be items that the inspector points out that you may have missed or just never considered. That doesn't mean the builder did something wrong, but it might mean there are things that could have been done better/different.

Step 6: Requests to Remedy

You had your inspection and now you have a big list of items that the home inspector pointed out. What do you do with that list? Foremost - Do Not Freak Out.

Every inspection comes back with a laundry list of items that are 'wrong' with the house. They aren't wrong, though, they just will need your attention and chances are 90% of them come up in 2/3s of all home inspections -it's not just your house, these issues are common to all homes that are being sold.

For the most part, this is your To-Do list for the first few years you own the home. Up until now you've thinking about paint colors and furniture placement as your to-do's but now you got to think about water run-off, flying splices and peeling paint.

This Is What We Ask The Home Seller To Take Care Prior To Your Purchase -> Anything that is unsafe or not working properly<-

There's a leak? It needs to be fixed.

The hot water heater isn't properly vented into the chimney and there is Carbon Monoxide venting into the basement? It needs to be taken care of.

Items that might fall into this category often involve electrical system issues - flying splices need caps, open junction boxes need covered, double tapped circuit breakers that aren't meant to be can be repaired, etc. This falls in the potentially unsafe category.

Electrical issues that might fall into the to-do list for future reference might include things like reverse polarity in an outlet, ungrounded outlets and active knob and tube wiring (I probably pointed out the knob and tube when we looked at the house but it is what it is, though insurance companies aren't fans) For the most part, old homes always have these type of issues, just be aware and take into future consideration.

On the other hand, you might as well include items like this on the Request to the Seller since they'll have an electrician out to repair the unsafe items anyway. Again, anything they take care of means you don't have to take care of it by expending your time, energy and money. This shortens your to-do list.

What do you NOT ask for? Chiefly, you don't ask for upgrades. The furnace is old? Yes, you saw that when you looked at the house, the sellers live there, the furnace works and does the job it's intended to do. Even if your inspector says its on its last leg, make a note of it. No Seller in their right mind would replace something that is working to their satisfaction with something new for you.

Not enough insulation in the attic? You don't ask the Seller to add more insulation, that'd be an upgrade as would installing a new asphalt driveway because (as you noted when you first visited) the current one is pretty old.

You don't have to buy the house as-is but you have to be reasonable. Again, unsafe and broken items are on your request to remedy for the Seller.

Radon

Speaking of unsafe, radon is a colorless, odorless gas that naturally occurs in the ground all over the world and causes thousands of cancer deaths in the United States each year. You should do a radon test. If the results come in above the EPA recommended safe levels, you should ask the Sellers to install a radon mitigation system in the home.

Step 7: The Appraisal

After you have agreed on remedies the seller will make if any I will let your lender know that they can order the property appraisal. The appraisal process typically takes about two weeks. The appraisal is ordered and is typically schedule anywhere from 5-7 days from the time of that I notify the lender that they can order it. Then it takes an appraiser between 5-7 days, sometimes longer to return the appraisal to the bank.

This is one of the last things that needs to happen to satisfaction for your bank to agree to move forward with underwriting your loan. If you are using a FHA or VA loan the appraiser will be looking a little deeper to make sure the home is in a superior condition. Items like peeling paint, cracked windows or a failing roof can fail an FHA or VA appraisal. If this happens then the seller must fix the items or the loan will not be able to proceed.

What if the appraisal comes in low?

This is happening more and more with the escalating multi-offer situations buyers are encountering. It’s not the best when an appraisal comes in low. The seller isn’t happy because your bank isn’t going to lend you the money for the amount you are in contract with them for. The seller may want to put the house back on the market and try their luck with another buyer and another appraiser. However, most of the time, seller’s don’t want to do all that and they will agree to lower the purchase price to the amount of the appraisal. Appraisals are there for a reason. In super competitive offer situations it is common to see an offer comes in with an ‘Appraisal clause’ stating that if the property does not appraise the buyer will bring the difference to the closing table in cash. I will never ask you to include this type of clause in a purchase contract. We will find a better deal on a different house!

Step 8: The Wait…

At this point in the home buying process you are just waiting for confirmation of your closing date. Some things you can do at this time include getting the info to change utilities over, shopping for home insurance and preparing your stuff for the move.

NOTE: DO NOT make any large purchases using your credit until you have CLOSED on the purchase of your home. Lenders run your credit right before going ‘clear to close’ on the loan and any new debt obligations can harm your ability to go through with buying the home you are in contract on!

Step 9: Closing Time

One last call for alcohol so bring me your whiskey or beer. Seriously though, most of the time, by the day of your closing you are ready for some whiskey, beer and maybe a vacation or three. Home buying is a somewhat lengthy process that is full of things beyond your control which can be VERY stressful. You may remember me saying this in the second paragraph of this whole guide. It’s true!

Leading up to the closing your lender and the title company will communicate with you about how much money you will need to have wired to the title company on the closing date. If you are married both spouses need to attend the close even if only one of you is on the loan as both of you will need to sign the closing documents. You will both need your ID’s for this. Typically closings happen in the office of the title company, however, all title companies are set up for remote closings so it could happen at my office or even the listing agents office if this proves to be more convenient for all involved.

You will sign many papers. Closings take between 30-90 minutes so they can be done before or after work relatively easily. I recommend you request your closing day off however, so you both can immediately leave the close and head to your new home.

Congratulations!! You have come to the end of my How-To Guide for Buying a home with me. If you have any questions feel free to mention them while we are doing showings. Thanks!

Matt Ward